GTA House Market Analysis

0. First Principles (Very Important)

1. High-Level Agentic Architecture

2. Data Ingestion Layer (Non-Negotiable)

2.1 Core Data Sources (Canada-specific)

3. Signal Extraction Agents (Deterministic)

3.1 Interest Rate Regime Agent

3.2 Supply–Demand Balance Agent

3.3 Price Momentum Agent

3.4 Affordability Stress Agent

4. Market Regime Classification Agent (LLM-Reasoning)

Role

Example Regimes

Input

Output

5. Bottom Detection Logic (Critical Part)

5.1 Define “Bottom” Explicitly

5.2 Bottom Signal Agent (Hybrid Logic)

6. Scenario Simulation Agent

Example Scenarios

7. Decision Agent (For You, the Buyer)

Inputs

Output (Actionable)

8. Continuous Learning Loop

9. Tech Stack (Concrete Suggestion)

10. What This System Will NOT Do (Be Honest)

Final Advice (Important)

Regions in Scope (Fixed)

1. System Philosophy (Critical for These Regions)

Region

Market Driver

Sensitivity

2. Data Layer (Region-Partitioned)

2.1 Mandatory Granularity

2.2 Key Regional Datasets

3. Regional Signal Agents (Parallel, Isolated)

3.1 Rate Transmission Agent (Regionalized)

3.2 Supply–Demand Imbalance Agent

3.3 Price Momentum & Drawdown Agent

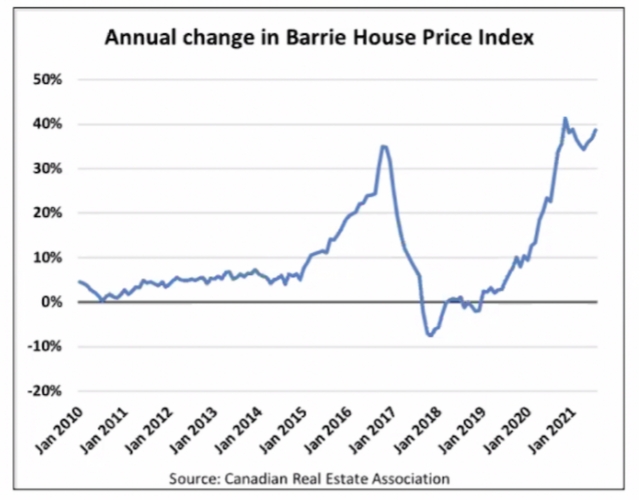

3.4 Speculation Flush Agent (Barrie-Specific Bias)

4. Regional Market Regime Agent (LLM)

Input

Output Example – Barrie

5. Bottom Detection Logic (Per Region)

5.1 Define Bottoms Separately

5.2 Buyer Advantage Agent (Core Agent)

6. Cross-Region Timing Arbitrage Agent

Insight

7. Scenario Generator (Region-Weighted)

Example Output

8. Final Decision Agent (You-Centric)

9. LangGraph Execution Model (Clean)

10. Hard Truth (Very Important)

Let’s focus on GTA alone then

Scope Locked

1. GTA Market Reality (Design Constraints)

2. Agent Stack Overview (GTA-Only)

3. Data Ingestion Layer (GTA Precision)

Mandatory Feeds (Monthly or Better)

4. Signal Agents (Deterministic, No LLM)

4.1 Rate Transmission Agent (GTA-Specific)

4.2 Inventory & Liquidity Agent

4.3 Price Momentum Agent

4.4 Affordability Compression Agent

5. Market Regime Classification Agent (LLM)

Input

Output

6. Plateau Detection Agent (MOST IMPORTANT)

Hard Conditions

Output

7. Buyer Leverage Agent (Decision Core)

Inputs

Output

8. Condo vs Freehold Split Agent

9. Final Decision Agent (Human-Readable)

Output Example

10. LangGraph Execution Model (Simple & Safe)

11. What This System Will Actually Tell You

Scope (Locked)

1. LangGraph State Schema (Single Source of Truth)

2. Node (Agent) Definitions

2.1 Ingestion Node (Deterministic)

2.2 Rate Transmission Agent

2.3 Inventory & Liquidity Agent

2.4 Price Momentum Agent

2.5 Affordability Compression Agent

2.6 Market Regime Classification Agent (LLM)

2.7 Plateau Detection Agent (Critical)

2.8 Buyer Leverage Agent

2.9 Segment Split Agent (Condo vs Freehold)

2.10 Final Decision Agent (LLM-lite)

3. LangGraph Topology

4. Guardrails (Non-Negotiable)

Hard Rules

Soft Rules

5. What This Graph Gives You (Real Value)

Prompt contracts for each agent

Prompt Contract Design Rules (Read First)

1. Market Regime Classification Agent (Primary Reasoning Agent)

Purpose

System Prompt

User Prompt Template

Required Output Schema

Hard Rejection Rules

2. Plateau Interpretation Agent (LLM-Light, Optional but Powerful)

System Prompt

User Prompt Template

Output Schema

3. Final Decision Narration Agent (Human-Facing)

System Prompt

User Prompt Template

Output Schema

4. Prompt-Level Safety Controls (Very Important)

Enforced at runtime:

5. Why This Prompt Design Works

Mathematical plateau formula

0. Definition (Be Precise)

1. Core Plateau Variables

Signal

Symbol

Meaning

2. Price Momentum Exhaustion (PME)

Inputs

Calculations

GTA Threshold

3. Inventory Stabilization (IS)

Inputs

Calculations

GTA Threshold

4. Sales Stabilization (SS)

Inputs

Calculations

GTA Threshold

5. Rate Pressure Neutralization (RPN)

Inputs

Calculations

GTA Threshold

6. Affordability Re-entry (AR)

Inputs

Calculations

GTA Threshold

7. Plateau Detection Formula (Final)

Boolean Plateau Gate

Plateau Probability Score

Decision Thresholds

Probability

Interpretation

8. Why This Works for GTA (Specifically)

9. Common False Signals (Guardrails)

10. How You Use This in Practice

Dashboard metrics (what to watch weekly)

GTA Housing Bottom Dashboard (Design Spec)

Core Principle

1. Dashboard Layout (One Screen)

2. Header: GTA Bottom Status (MOST IMPORTANT)

Widget: Status Banner

3. Plateau Probability Gauge

Widget: Horizontal Gauge (0 → 1)

4. Buyer Leverage Panel (Your Negotiation Power)

Metrics

Composite Score

Thresholds

Score

Meaning

5. Inventory Stabilization Panel

Charts (Small Multiples)

Visual Cue

6. Price Momentum Panel (Anti–False Bottom)

Charts

Threshold Line

7. Rates Panel (Silent Killer)

Metrics

Signal Lamp

8. Affordability Re-Entry Panel

Metrics

Interpretation Zones

Zone

Meaning

9. Condo vs Freehold Toggle

10. Weekly vs Monthly Cadence (Important)

Metric

Frequency

11. Alerts (Minimal, High Signal)

12. What This Dashboard Prevents

13. Final Operator Rule (Memorize This)

Buy vs Rent - break-even logic

Part A — Monte Carlo Downside Simulation (GTA-Specific)

What This Is (and Is NOT)

1. What You Simulate (Minimal, Sufficient)

2. Parameterization (Grounded, Conservative)

Shock

Probability

Impact

3. Simulation Engine (Pseudo-code)

4. Outputs That Matter (Only These)

Metric

Meaning

5. How This Feeds Decisions

Part B — Weekly Decision Report (Human-Consumable)

1. Report Cadence

Component

Frequency

2. One-Page Report Structure

3. Tone Rules (Critical)

How This Completes the System

A. Integrating Monte Carlo as a Gated LangGraph Node

Why a gated node?

1. Where the Monte Carlo Node Sits

2. Gate Condition (Very Important)

3. LangGraph Node Definition (Pseudo-code)

4. Monte Carlo Output Contract (Strict)

5. Decision Agent Override Logic

B. Auto-Generated Weekly Decision Memo

1. What the Memo Is

2. Memo Generation Agent (LLM, Read-Only)

3. Memo Agent Input (Structured Only)

4. Memo Prompt Contract (Key Excerpt)

5. Memo Structure (Fixed)

6. Output Format

Why This Matters More Than Anything Else

Final Mental Model (Keep This)

Add a personal regret-minimization score

What “Regret-Minimization” Means (Operationally)

Regret Is Personal (Not Market-Based)

The Regret-Minimization Score (RMS)

High-level idea

Step 1 — Quantify “Regret of Buying Too Early” (R_buy)

Inputs (already in your system)

Formula

Step 2 — Quantify “Regret of Waiting Too Long” (R_wait)

Inputs

Formula

Step 3 — Normalize & Compute RMS

Interpretation

RMS Range

Meaning

Action Bias

Step 4 — Hard Safety Gates (Still Apply)

Where RMS Fits in Your LangGraph

Regret Node Output Contract

Why This Is Extremely Powerful

Example (Concrete)

Final Mental Model (Keep This)

Concrete, month-by-month walkthrough of how the Regret-Minimization Score (RMS)

Key Reminder (What RMS Measures)

Assumptions for the Walkthrough (Fixed)

Month-by-Month Near a Plateau

Month T-2 — Late Decline (Too Early)

Month T-1 — Early Plateau Formation

Month T — Plateau Confirmed (Asymmetry Flips)

Month T+1 — Early Recovery (Too Late for Comfort)

Month T+2 — Post-Plateau (Emotionally Hard)

Visual Summary (Mental Model)

Why This Is Extremely Important

Final Rule (Memorize This)

How the RMS timeline is embedded into the weekly memo

What “Plug RMS Timeline into the Weekly Memo” Actually Means

1. RMS Is Tracked as a Time Series (Not a Snapshot)

2. RMS Section in the Weekly Memo (Fixed Placement)

Section Title (always present)

3. RMS Summary Block (Quantitative but Human)

4. RMS Timeline Indicator (Very Important)

5. “What Changed in Regret” (Delta-Driven)

6. RMS → Decision Bias Mapping (Explicit, Not Implied)

7. RMS-Based Forward Guidance (Trigger-Oriented)

8. Full Weekly Memo Excerpt (Concrete Example)

9. Why This Is So Powerful (Practically)

Final Mental Rule (Pin This)

Integrate RMS into the LangGraph decision node

1. What RMS Is Allowed to Do in LangGraph

2. Where RMS Lives in the Graph (Exact Placement)

3. RMS Node: Inputs and Outputs (Contract)

Inputs (Read-Only)

Outputs (Strict)

4. The Final Decision Node (This Is the Key Part)

RMS modifies this baseline only within bounds

Translation into English

5. Why RMS Is Not Redundant with Monte Carlo

Tool

Answers

6. Example: Same Market, Two Outcomes (Correctly)

Market State (Same)

Person A

Person B

7. Why This Integration Is the “Last 5%”

Final Takeaway (One Line)

Single LangGraph decision table

GTA LangGraph — Final Decision Table

1. Inputs (All Pre-Computed Upstream)

Variable

Meaning

2. Decision Table (Authoritative)

Priority

Condition (ALL must be true)

Action

Rationale

3. Visual Hierarchy (Important)

4. How This Maps to LangGraph Code

Decision Node (Pseudo-Code)

5. Why a Decision Table Beats “Agent Reasoning”

6. One-Line Interpretation Guide

Final Rule (Pin This)

Kiro Requirements

📄 KIRO REQUIREMENTS

Project: GTA Housing Market Bottom Detection & Buy Decision System (Agentic GenAI)

1. Objective

2. Scope (Strict)

Geography

Property Focus

Time Horizon

3. Core Principles (Non-Negotiable)

4. System Architecture (High Level)

5. Data Requirements

Market Data (Monthly)

Rate Data (Weekly)

Demand & Stress

6. Deterministic Signal Agents (No LLM)

Required Agents

7. Market Regime Classification Agent (LLM)

Purpose

Allowed Regimes

Allowed Cycle Stages

Constraints

8. Plateau Detection (Mathematical Core)

Signals (Binary)

Plateau Condition

Plateau Probability

Thresholds

9. Buyer Leverage Scoring

Inputs

Output

Interpretation

10. Monte Carlo Downside Simulation (Gated)

Purpose

Run Conditions

Outputs

Hard Gate

11. Regret-Minimization Score (RMS)

Purpose

Formula

Interpretation

RMS may:

12. Final Decision Policy (Authoritative Table)

Priority

Conditions

Action

13. Weekly Decision Memo (Human Output)

Characteristics

Required Sections

14. LangGraph Requirements

Graph Properties

Node Types

State Object

15. Non-Goals (Explicit)

16. Success Criteria

17. Expected Output from Kiro

Final Instruction You Can Give Kiro

Product Requirements Document (PRD)

Product Requirements Document (PRD)

Product Name

Geography

1. Purpose & Vision

1.1 Problem Statement

1.2 Product Vision

2. Goals & Non-Goals

2.1 Goals

2.2 Non-Goals (Explicit)

3. Target User

Primary User

Secondary Users

4. Core Product Principles (Hard Constraints)

5. System Overview

5.1 High-Level Architecture

6. Data Requirements

6.1 Market Data (Monthly)

6.2 Rate Data (Weekly)

6.3 Demand & Stress Indicators

7. Deterministic Signal Layer (No LLM)

Required Agents

8. Market Regime Classification (LLM)

Purpose

Allowed Regimes

Allowed Cycle Stages

Constraints

9. Plateau Detection (Mathematical Core)

Binary Signals

Plateau Condition

Plateau Probability

Interpretation

Probability

Meaning

10. Buyer Leverage Scoring

Inputs

Output

Interpretation

11. Monte Carlo Downside Risk Simulation

Purpose

Execution Conditions

Outputs

Hard Risk Gate

12. Regret-Minimization Score (RMS)

Purpose

Definition

Interpretation

RMS

Bias

13. Final Decision Policy (Authoritative)

Priority

Conditions

Action

14. Weekly Decision Memo (Primary Output)

Characteristics

Required Sections

15. Technical Constraints

16. Success Metrics

17. Deliverables

Final Instruction for Execution

Last updated